Taos Real Estate Market Report

January – March 2026 (3 months)

For the first 3 months 2026 vs. 2025, the number of sales of Single-family Homes was up; Condos and Land sales were down; Multi-family Housing and Commercial sales were the same as last year.

Single-Family Home sales continued the uptrend that started in 2025 (after declines in 2023 and 2024). Condo sales have been in a downtrend since 2022. Land sales continue to fall as high building costs are making home building less attractive. Multi-family sales are nil through Q1 (same as last year), as investors for this type of property are impacted by higher interest rates. Commercial investments are likewise negatively affected by current interest rates, as well as by concerns about the strength of the economy.

The uncertainty that pervaded the real estate market in 2025 persists. The military conflict in Iran has added another layer to concerns about inflation and consumer price, interest rates, and the health of the job market and the economy. People remain cautious about investing in real estate. In Taos, most real estate purchases are discretionary (i.e., people don’t need to buy), and many prospective buyers are waiting to see how things develop. This is in sharp contrast to the buyer psychology of 2020-2022, when people were eager to buy real estate despite negative news.

HOWEVER — The long-term trend for Taos remains positive. This community will continue to draw people for whom the wonderful climate, amazing natural beauty, abundant recreational opportunities, vibrant cultural scene and laid-back lifestyle make it an attractive place to live.

Click each title below to view the discussion and data for that property type.

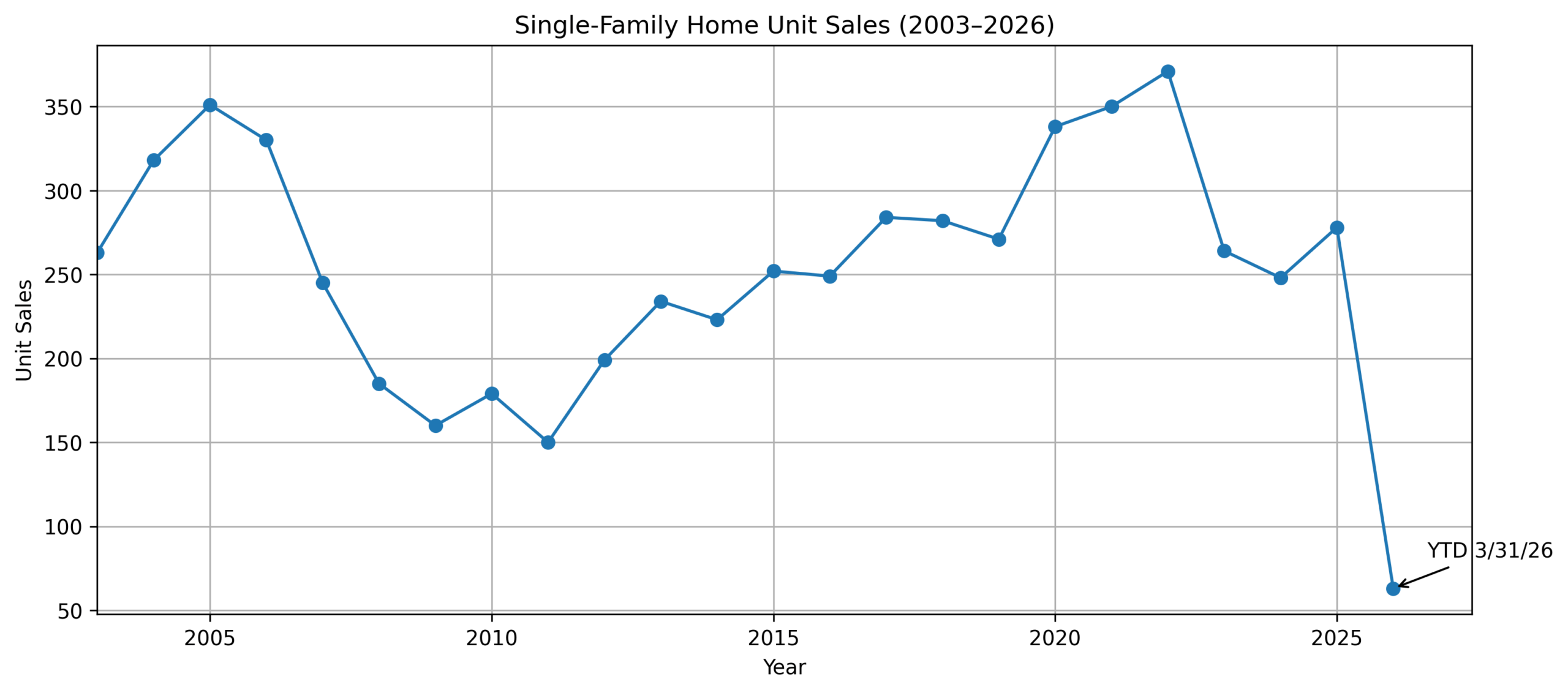

The number of sales is up, but prices are not.

For January through March, unit sales were 63 this year vs. 57 last year, an increase of 6 sales (+10.5%). But dollar sales were down by 3.8%. Median price declined 11.8%, and average price was off 12.8%.

The market boomed during the Covid pandemic buying frenzy that started in 2020 and peaked in 2022. Sales then fell for two years, bottoming out in 2024. In 2025, the market turned up and the uptrend has continued in 2026 although it’s far from the red-hot market of 2020-2022. The are fewer people actively looking to buy, while the inventory of homes available for purchase has increased significantly. As a result, the severe imbalance between supply and demand that existed during the boom has moderated. Buyers have more homes to choose from—and more room to negotiate price and terms. If they don’t find a house they really like and at a price they think is reasonable, they don’t buy. During the boom almost everything in reasonably good condition and location was selling at full asking price–or higher. There were often multiple offers. Now, buyers are more selective about a home’s features, location and condition—and more value conscious. Mutliple offers and bidding competitions are no longer common.

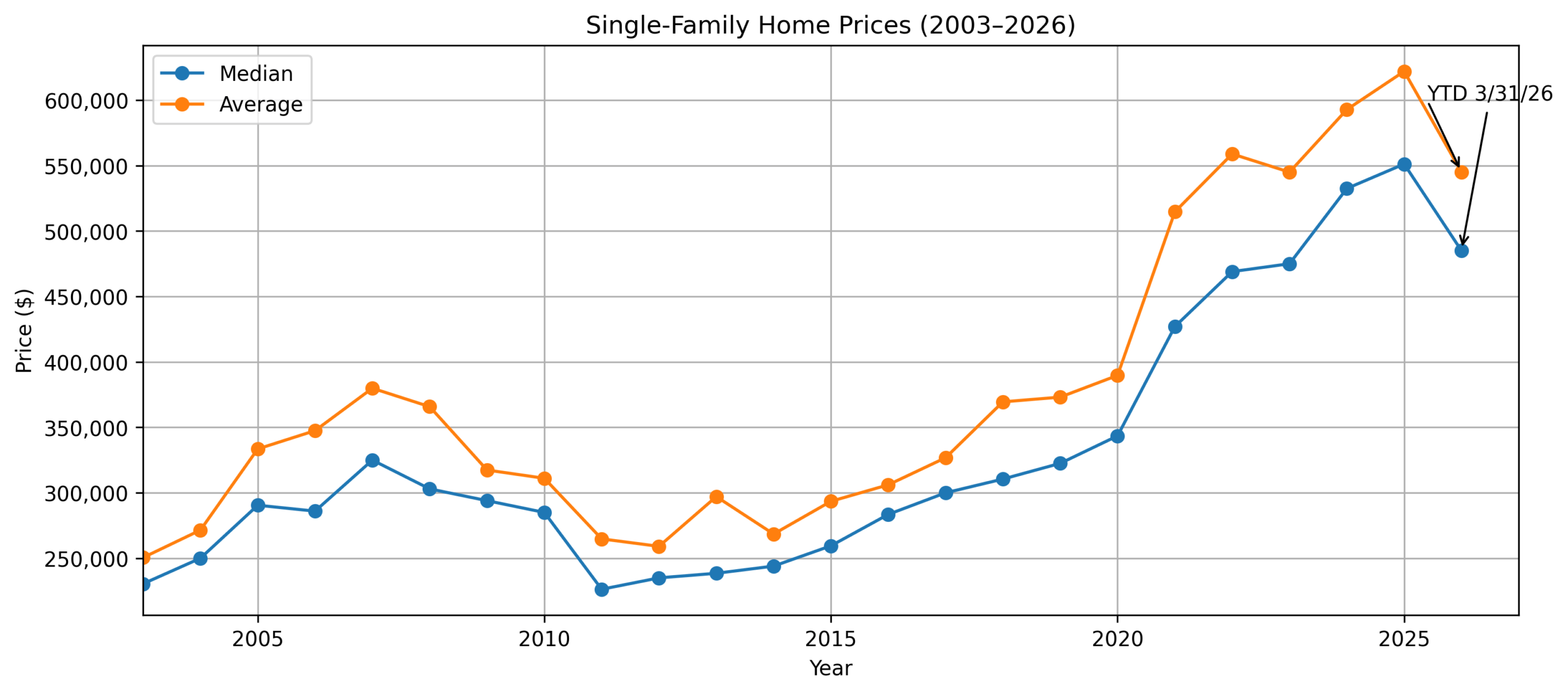

MEDIAN AND AVERAGE PRICES

2026 Q1 median price (midpoint in the range of sales prices from lowest to highest) was $485,000, a decrease of $65,000 (-11.8%) from $550,000 in 2025 Q1.

The average (mean) price was $545,000 vs. $625,000, a decline of $80,000 (-12.8%).

Here is how median and average prices have changed since 2003:

Prices surged during the 2020 – 2022 boom. During those years, the median price jumped 37%, almost 20% per year. From 2020 to 2025, the median increased 60% and average price gained 56%. Looking further back, from 2016 to 2025, the median has almost doubled! At this point, it appears that prices are not rising. It is too early to say that they are actually falling but they may be, as buyer demand remains weak while supply increases. We should have a better sense of the price level after the second quarter.

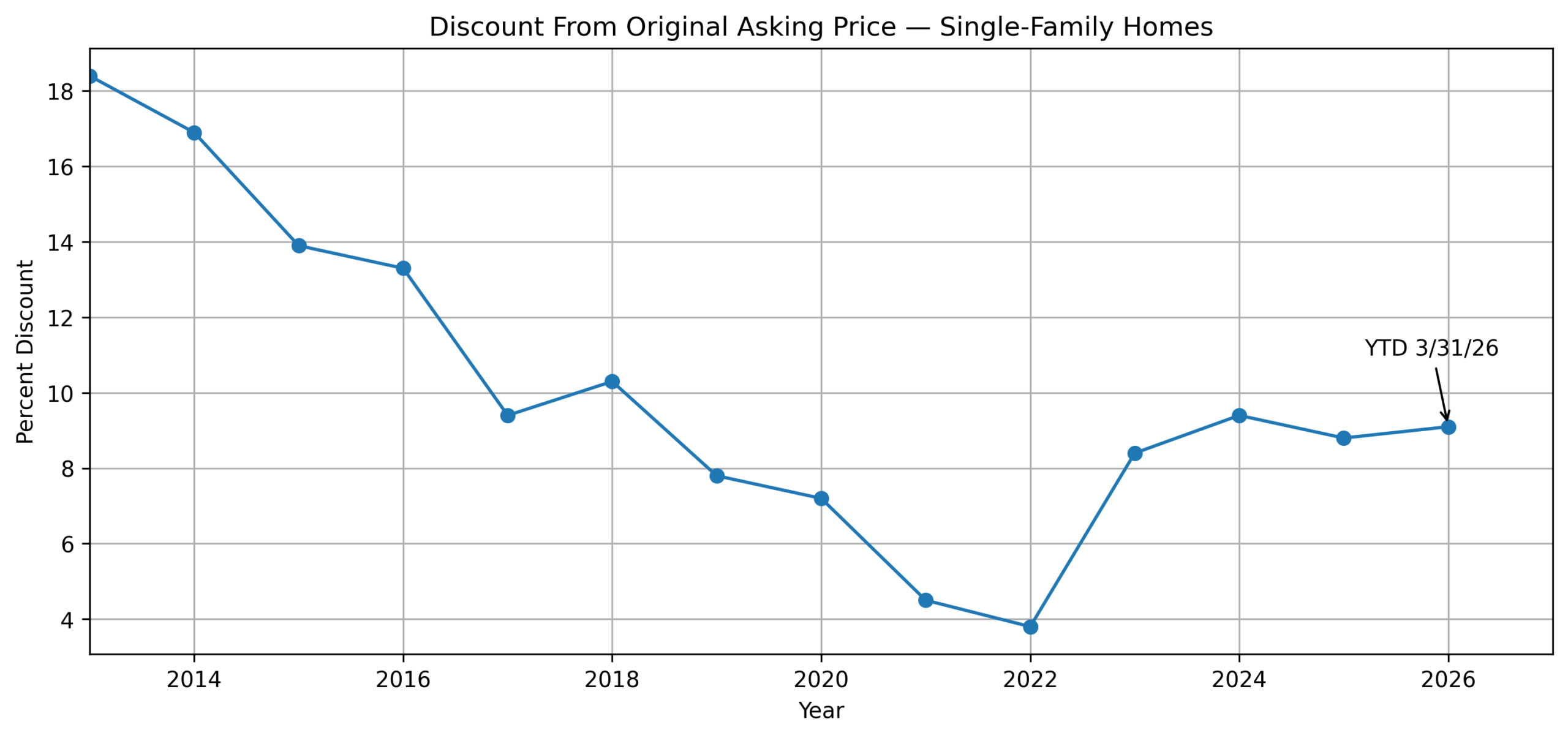

PRICE DISCOUNTING

For the 63 sales closed in the first quarter this year, final sales price averaged 5.1% less than the asking price when the home when under contract; however, it was 9.1% less than the initial asking price when the home was first listed. For the full year 2025, these discounts were 5.1% and 8.8% respectively. The chart below shows that the discounts were lowest in 2022 at the height of the boom, and have been trending higher since then. Homes that are priced as if the market is as strong as it was in 2020-2022 are taking longer to sell, and often go through one or more price reductions before they sell.

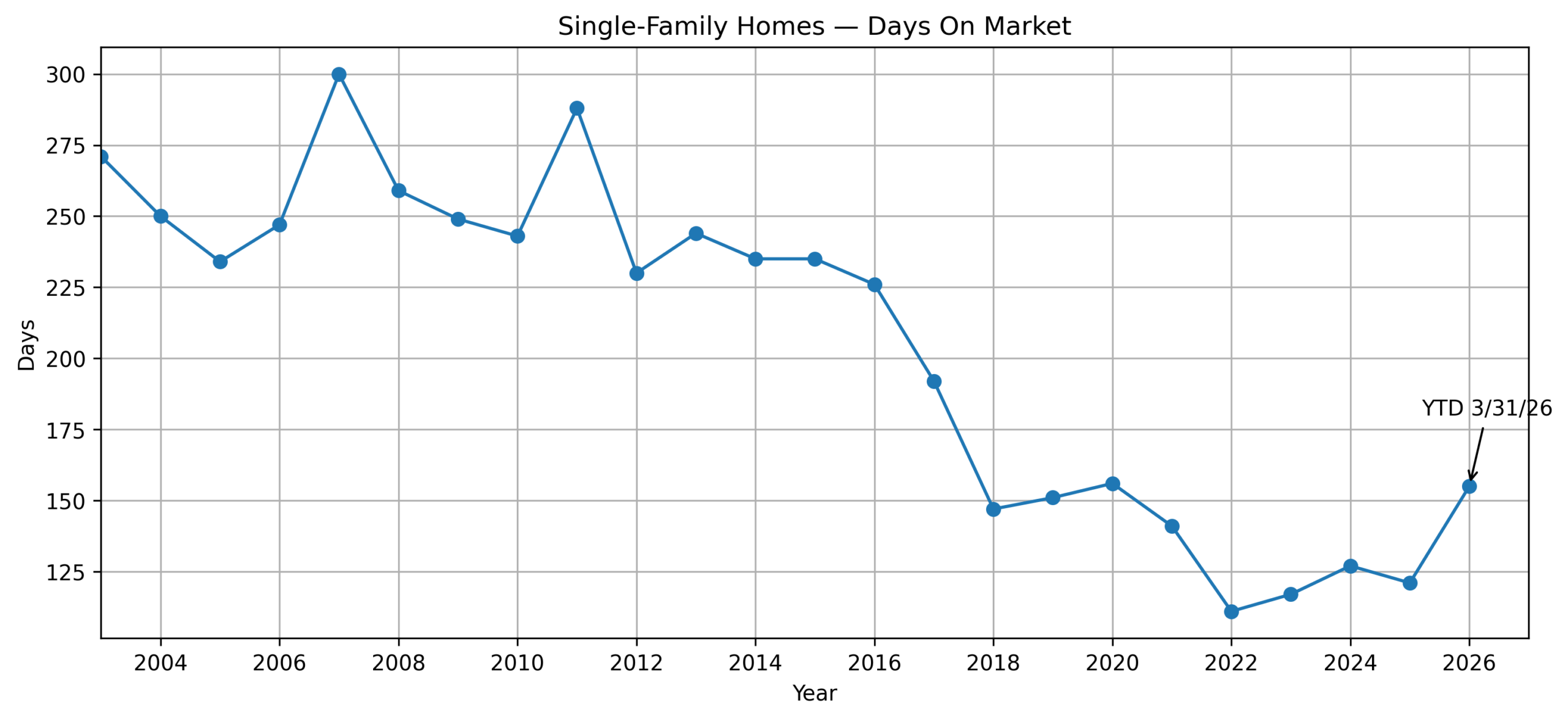

DAYS ON MARKET

For 2026 Q1, the average number of days from the start of a listing to when the house went under contract was 155, an increase of 11 days from the same time peiod in 2025. Full-year 2025 DOM averaged 121; in 2024 it was 127. DOM started trending down in 2011 as demand began to outstrip supply. It reached a low point in 2022, and has been trending higher since then. In Taos, average time to sell has always been much higher than in many parts of the country—where homes typically sell in 30-45 days in normal times. For the years 2003 – 2016, in Taos it took an average of 250 days for a house to sell.

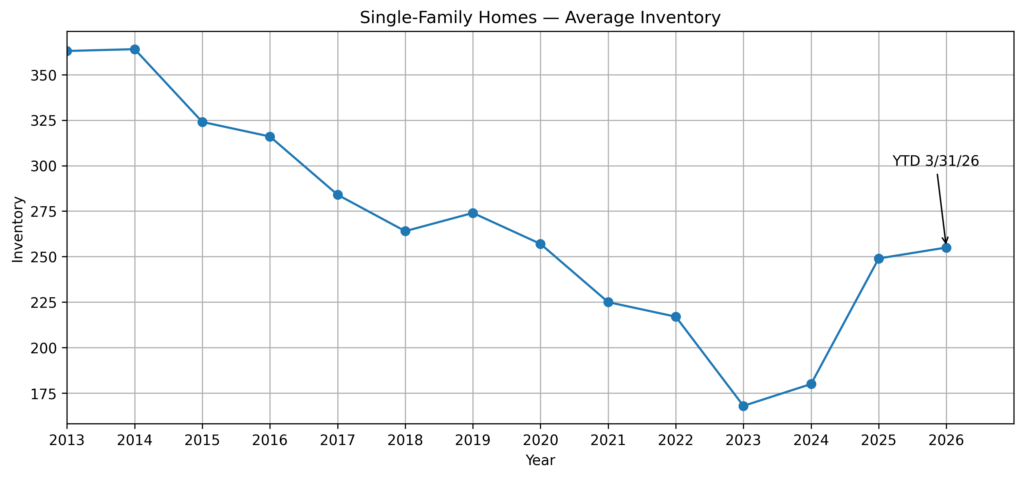

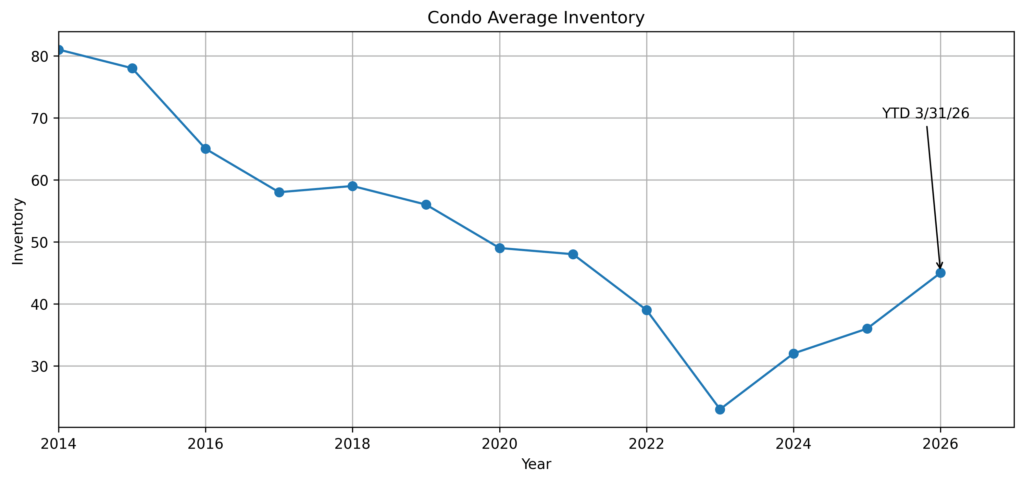

INVENTORY

The supply of homes available for purchase has continued to increase from a low point in 2023. At the time this report was prepared, there were 260 homes listed for sale, up 6 houses (+37%) from 3 months ago, and up 42 (+19%) from a year ago. It appears that more homeowners are deciding that it is time to sell even if it means giving up their ultra-low mortgage loan interest rates. Inventory is expected to increase further as we get into the main Taos selling season of summer and fall. Supply and demand are more in balance than they were a few years ago. It has become somewhat easier to find more than just a few homes to show a buyer that meet most of his/her criteria. Nevertheless, Taos inventory consists of a wide variety of style, size, location, condition and price, so it’s still unlikely to find 10 homes to show a buyer. Inventory is still far below what was typical in the years before the 2009 real estate market collapse. For example, in September of 2008, there were 518 homes listed for sale! The graph below shows how average inventory plummeted to a low point in 2023 during the Covid pandemic boom.

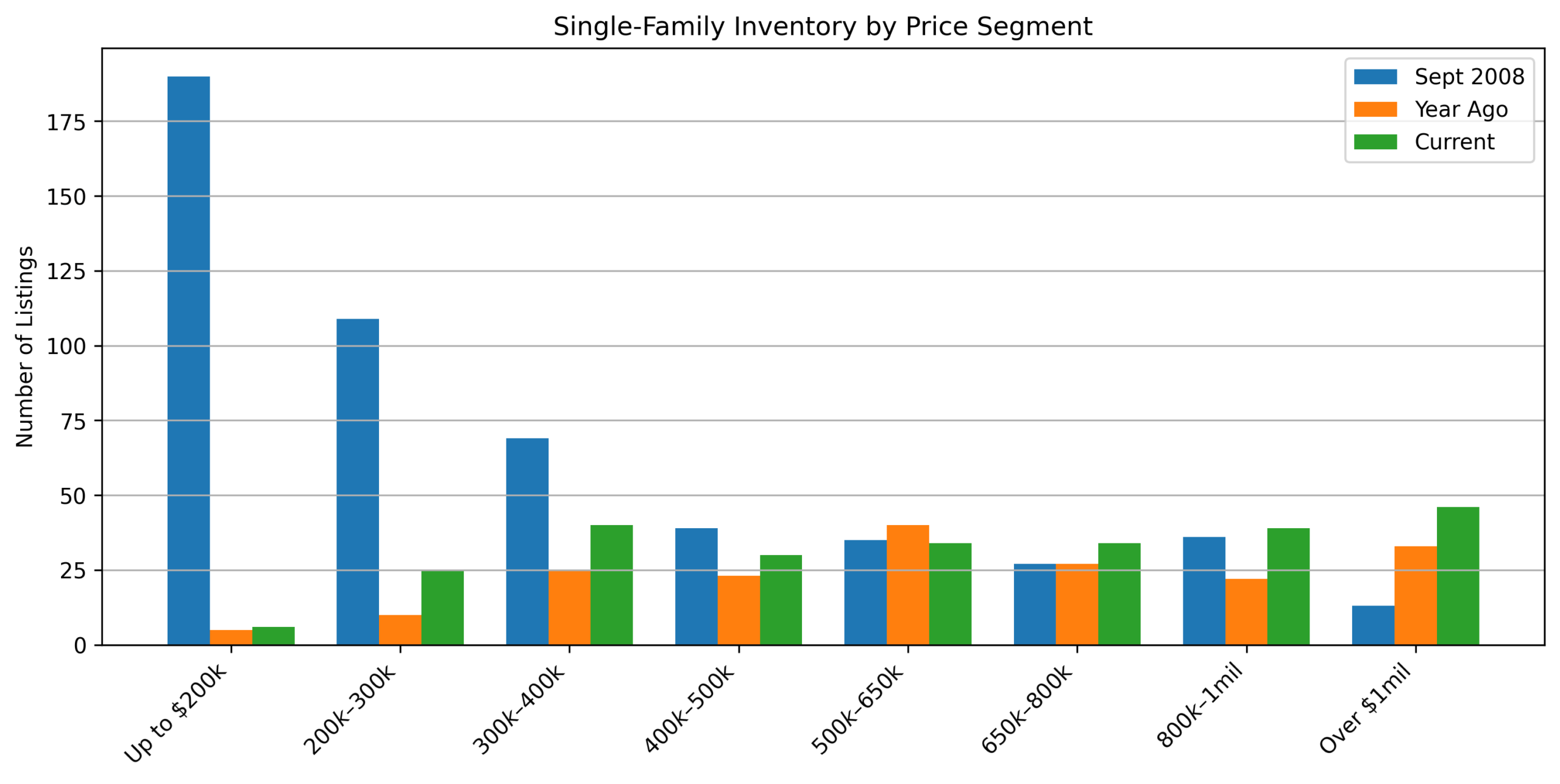

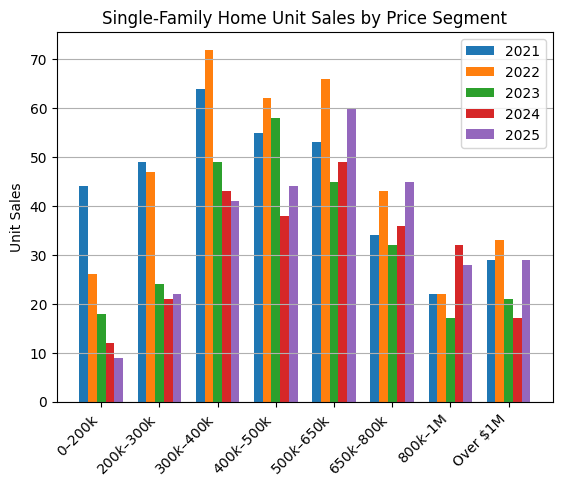

The two graphs below illustrate how the number of homes available for purchase in the lower price segments has dwindled, and the corresponding increase in sales of higher-priced homes. This is a result of the huge rise in the overall price level. A home that had a value of $350,000 pre-Covid is now worth probably $575,000.

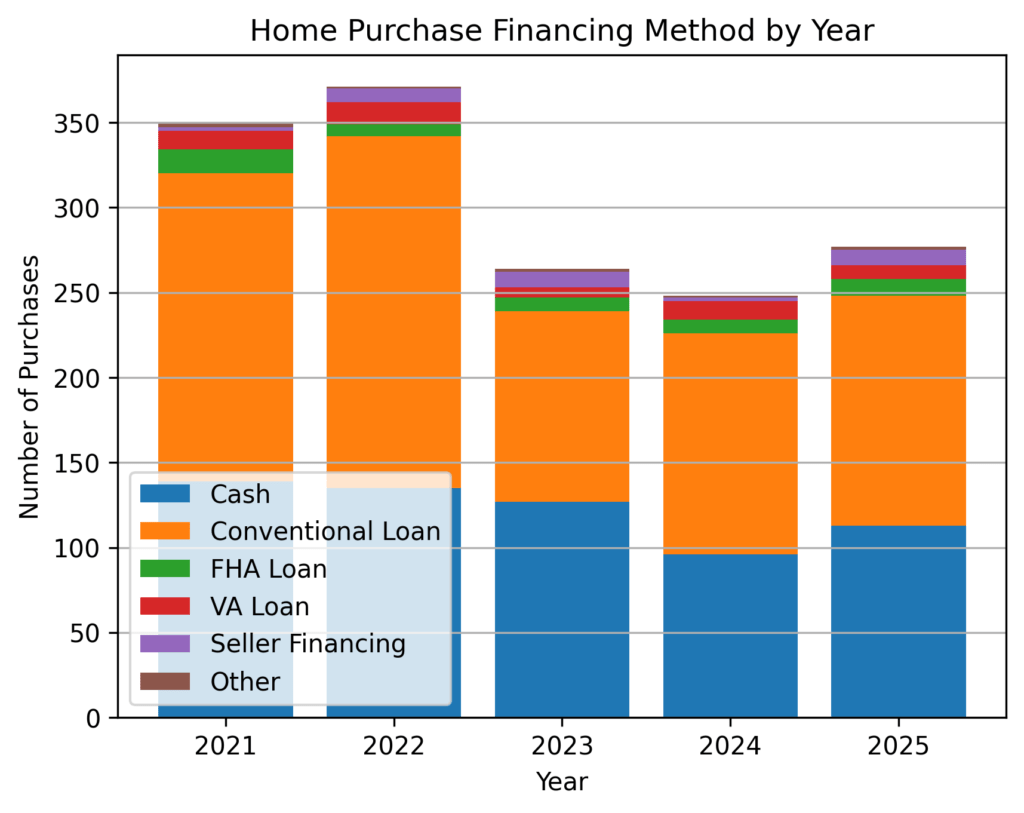

This bar chart shows that cash purchases are still a large percentage of total sales.

INTEREST RATES

The 30-year fixed rate loan was averaging 6.30% at the time of this report’s writing. That is up from 6.09% three months ago, but down from just over 7% in January 2025. The war in Iran has caused the oil price to spike, which in turn will probably push inflation back up. The expectation of higher inflation along with concern about ballooning government debt will probably cause the interest rates on long-term debt to rise. Mortgage rates are generally linked to the rate on 10-year Treasury notes; mortgage rates probably stay above 6% and they may go back up to 7% — unless there is a recession.

By now most people realize and accept that mortgage rates are not ever going back down to the super-low levels that occurred during 2009-2021. Those rates were created by the government’s “quantitative easing” program to prevent a possible depression after the Global Financial Crisis of 2008. The Covid pandemic was another reason to keep rates suppressed and to flood the financial system with excessive liquidity. Ultra-low interest rates caused asset prices (including real estate) to rise dramatically.

Some people may not remember that 6%-7% was a very normal mortgage rate for many years before 2008. Here is a link to the Federal Home Loan Mortgage Corporation (“Freddie Mac”) web site where you can see rates going back to the 1970’s: https://www.freddiemac.com/pmms

| Conventional 30-year fixed | 6.30% |

| Conventional 15-year fixed | 5.65% |

Note: Interest rates are impacted by occupancy, credit score, and down payment.

FORECLOSURE SALES

In the first 3 months of 2026, there was one foreclosure sale. In each of the years 2023, 2024 and 2025, there were but 4 foreclosure sales; in 2022 there were none. The number of foreclosures diminished steadily from a peak of 55 in 2012 during the aftermath of the Great Financial Crisis of 2008-2009. Currently, there are only two bank-owned houses listed for sale. One is an 11,000-square foot house on 10 acres listed at $2.2 million.

Please Note: These data do not include any condominiums developed or offered for sale by Taos Ski Valley Resort; those condos are not listed in the Taos MLS.

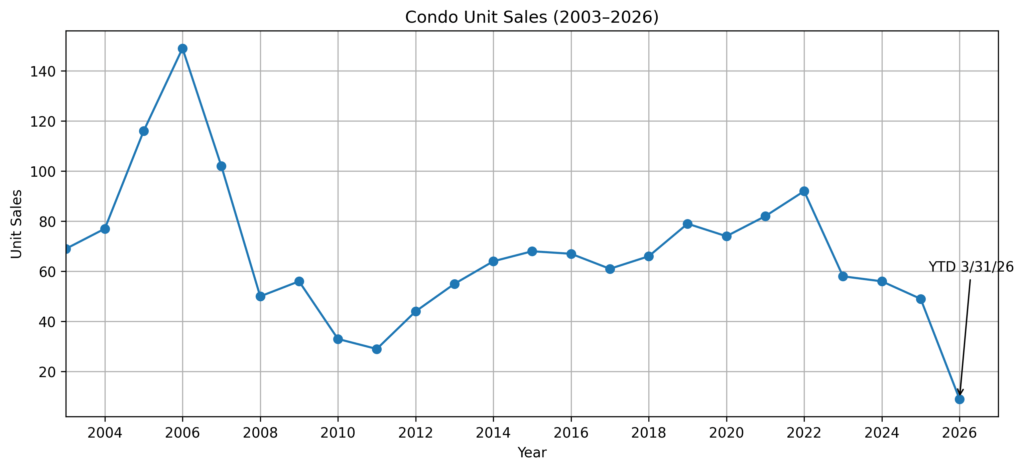

Condo sales are still trending downward.

For the first 3 months of 2026, the number of closed sales was 4 fewer than in 2025Q1, at 9 vs. 13 sales (-30.8%). Condo sales have been lackluster since 2022. Limited inventory is part of the reason; but there just doesn’t seem to be much interest in condos these days.

Dollar sales for the first quarter were down 32.9%. The median price was actually up, but average price was down. Note: 9 sales is not sufficient data to accurately gauge a trend. Total sales and average prices are affected by the “sales mix”—the comparative number of higher- and lower-priced units sold.. Of the 9 condos sold in 2026 Q1, only 1 was at Taos Ski Valley (where prices tend to be substantially higher than in town); in 2025 Q1, 4 out of the 13 sales were at TSV.

The high-water mark for Condo sales was 2006, when 149 units sold. There was much more inventory for buyers to choose from back in the early 2000’s, and there was more buyer interest in condos. After 2006, sales dropped to 29 in 2011, then gained slowly up to a high point of 92 in 2022. Since then, they have been drifting steadily downward.

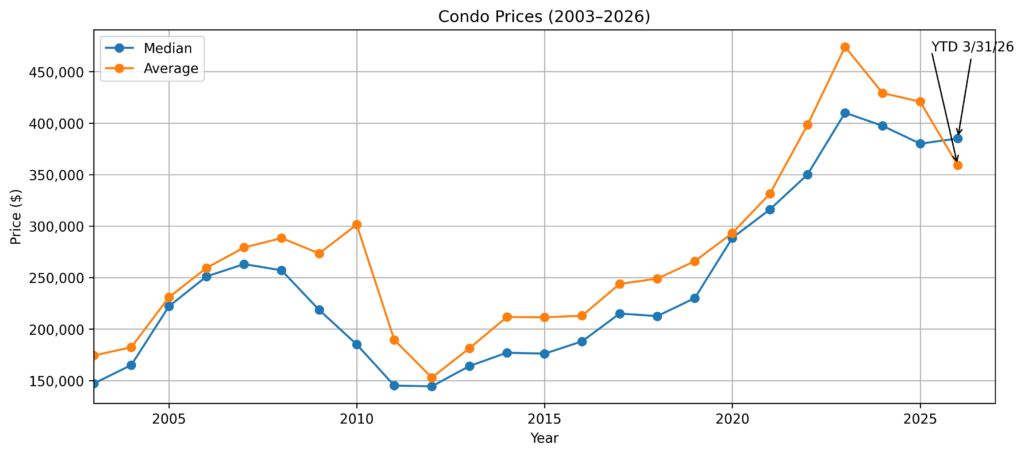

MEDIAN AND AVERAGE PRICES

Median price for the 2026 Q1 was $385,000 vs. $350,000 in 2025 Q1, a gain of $35,000 (+10.0%). Average price was $359,000 vs. $370,200, a decrease of $11,200 (-3.0%). In full-year 2025, the median was $380,000 vs. $397,300 in 2024, a decline of $17,300 (-4.4%); average price last year was $420,800 vs. $429,100 in 2024, a loss of $8,300 (-1.9%). As noted above, a data set of only 9 sales so far this year is not enough to form an opinion on the direction of condo prices; however, It seems fairly clear that condo prices are weak.

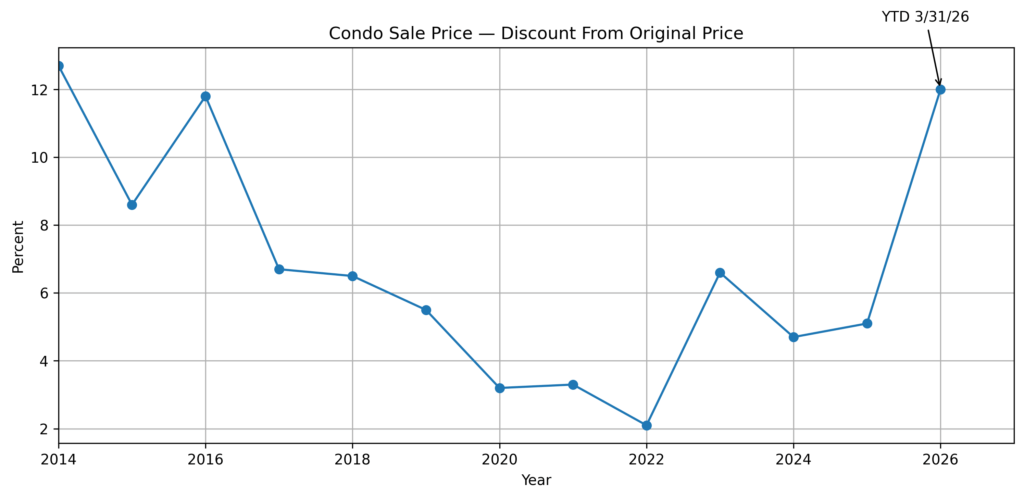

PRICE DISCOUNTING

First quarter sales prices in 2026 averaged 4.3% less than the asking price when the condo went under contract. The discount from original price when the condo was first listed was 12.0%. For full year 2025, final sales price averaged 3.3% less than the asking price when the property went under contract, and 5.1% below original listing price. Full-year 2024 discounts were 3.0% and 4.7%, respectively. The upticks in price discounting indicate that the condo market is soft.

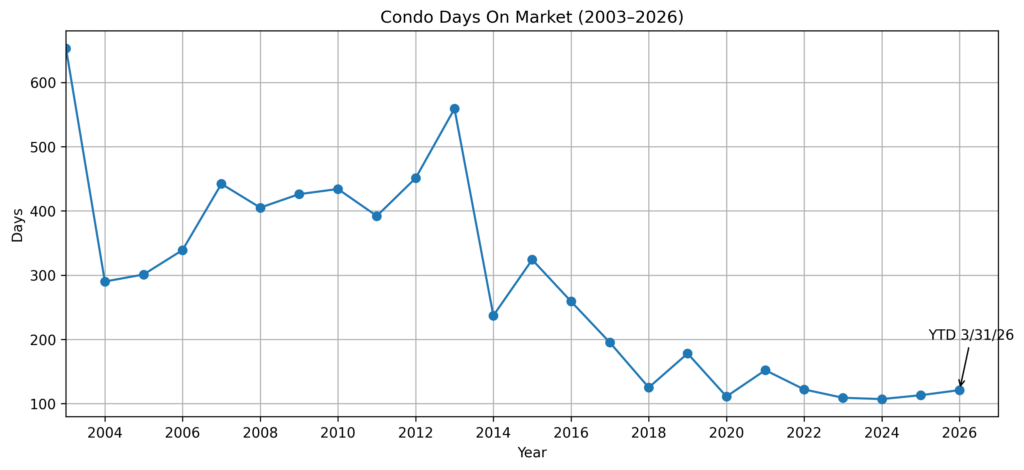

DAYS ON MARKET – For 2026 Q1, DOM increased to 121 from 107 in 2025 Q1 (+13.1%). Again, there is not enough data yet to be able to conclude that DOM are trending upward.

INVENTORY

The number of condos listed for sale at the time of this report was 49, up 7 from three months ago. Of the 49 condos currently listed for sale, 12 are at Taos Ski Valley; 37 are in or near central Taos. Those 37 available condos in Town range in price from $205,000 for a 503-square foot 1-bedroom/1-bath unit in central Taos to $675,000 for a 2BR/2BA unit of 1,339 sq. ft unit, with a 2-car garage, also close to Town center.

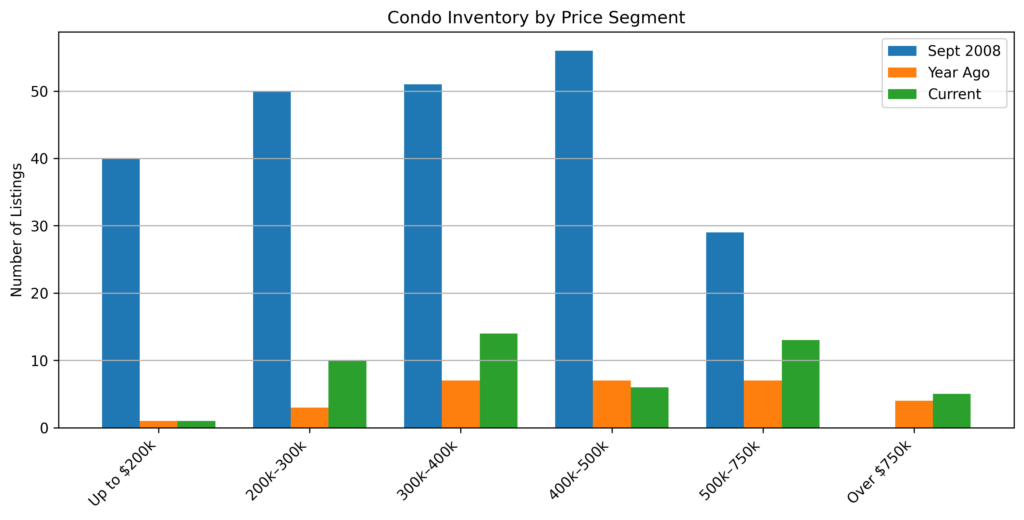

In 2005-2006, when condo development was at its peak, there were often approximately 200 condos on the market at any given time, with the majority in or near central Taos. There were 149 condos sold in 2006. The table below shows a steady decrease in average inventory for each year from 2013 to 2023, and not much increase since then There hasn’t been much developer interest in building new condos.

Here is Condo Inventory by Price Segment comparing Current with a Year Ago and with Sept 2008 when inventory peaked:

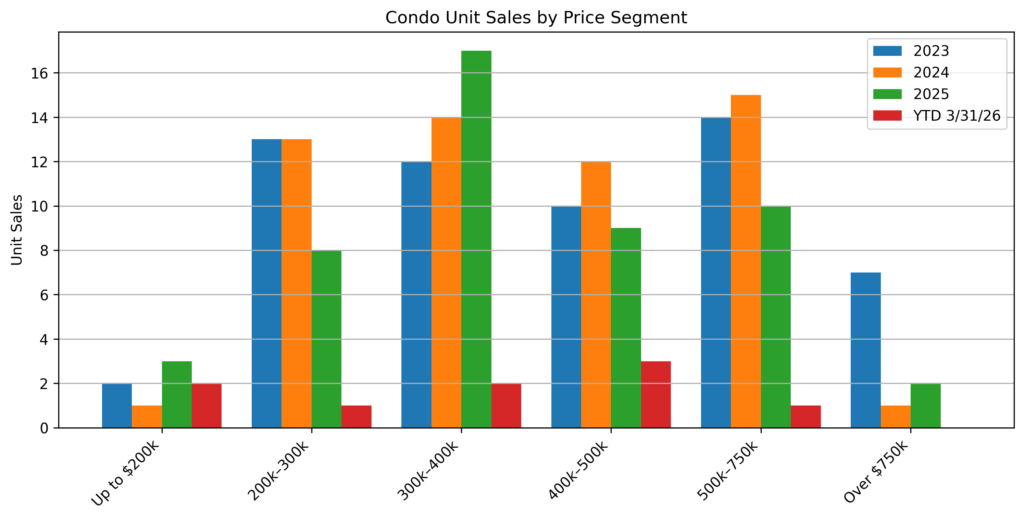

The following bar chart shows Condo unit sales by Price Segment:

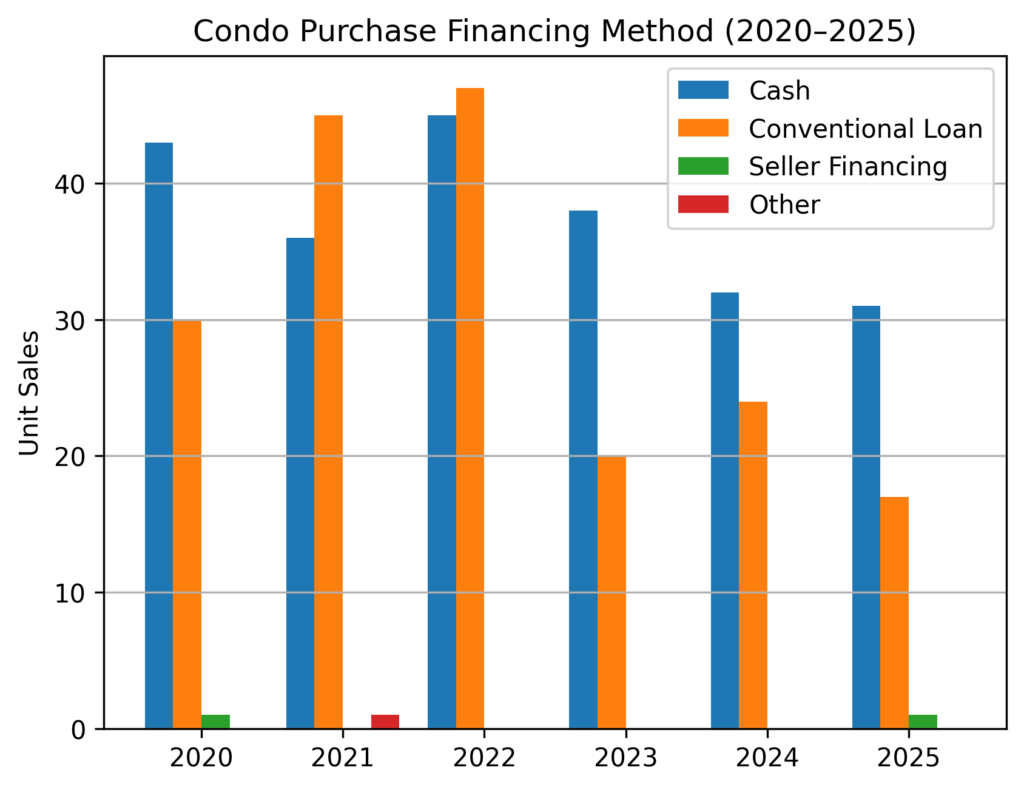

This bar chart shows that loans were a higher proportion than cash during 2021 and 2022 when interest rates were ultra-low, and loans were easy to get:

FORECLOSURE SALES

There have been no foreclosure sales so far in 2026. There haven’t been any since 2019, when there was only one.

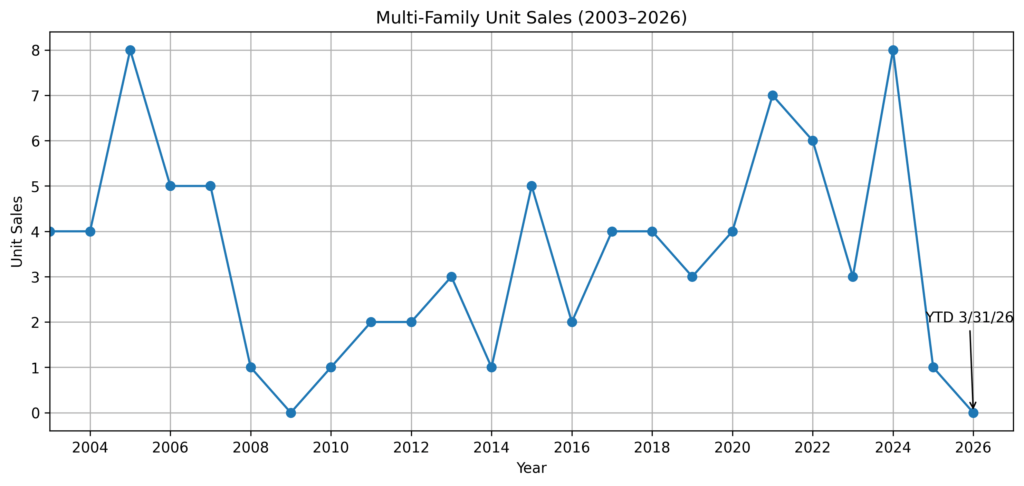

There have been no sales of Multi-family property so far in 2026.

The first quarter of last year also had zero sales. 2025 ended the year with just 2 sales, a steep drop from 8 in 2024. Weakness in this market segment is no doubt due to higher interest rates affecting investors’ ability to achieve a satisfactory rate of return.

In an economy of higher interest rates, investors normally require higher “capitalization rates” to evaluate real estate investments. Investors divide a property’s Net Operating Income by their desired cap rate (their required rate of return expressed as a percentage) to calculate the price they can pay to achieve the target rate of return. For example, if a property generates Net Operating Income of $25,000 per year, a cap rate of 5% means a value of $25,000/5% = $500,000; a cap rate of 8% gives a value of $312,500

There is huge need for affordable housing, and Multi-family would be a large part of that; but “making the numbers work” in Taos has always been a challenge. For new construction, the high cost of land in suitable locations combined with high costs for materials and labor, make it difficult to achieve a reasonable rate of return. Additionally, most multi-family properties listed for sale are small (typically 2- 4 units); therefore, management expenses further reduce Net Operating Income.

Multi-family has always been a very small segment of the Taos real estate market; it will remain so, at least in the near future. Currently, there are 15 multi-family listings for sale; two have pending sales (both are duplexes)

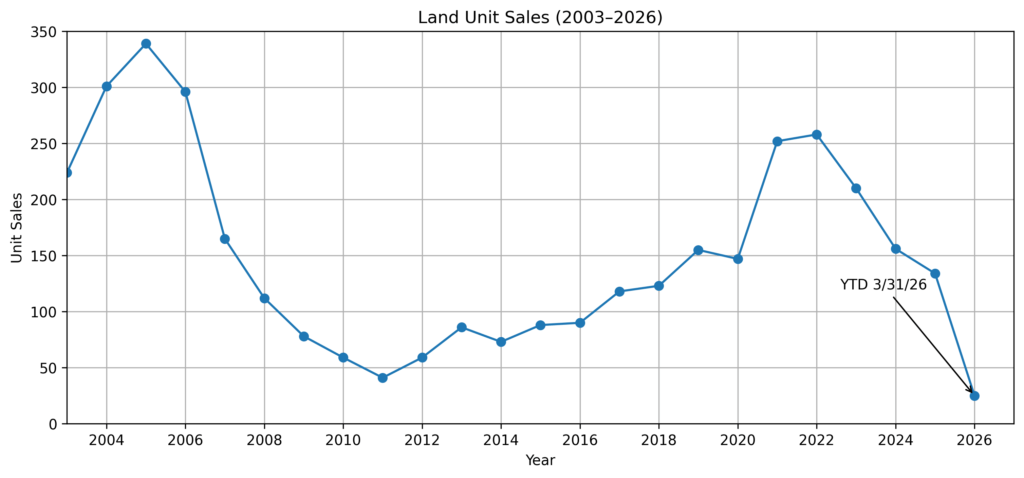

Land sales continue a downward trend.

2026 first quarter number of sales was 25 vs. 36 in 2025 Q1, a drop of 11 (-30.6%). Dollar sales were down 60.7%, as both median and average prices fell.

Since a brief rally in 2021-2022 during the Covid pandemic boom market, sales have diminished each year.

The primary constraints on land sales are very high building costs and the long lead time to start and complete construction of a home. There aren’t a lot of really good custom home builders working in Taos, and they are booked up for about two years. For a good-quality home (but not a really high-end one) it costs more than $400 per square foot for the hard dollar cost of construction. This doesn’t include the land purchase, design, possible well drilling, septic system installation, and landscaping. The likelihood that costs will remain high will continue to be a drag on land sales. And with the supply of existing homes for sale increasing, buyers have even more reason to forego building a new home.

Back in peak year 2005, when there was a lot of interest in land and building costs were more reasonable, there were 339 closed sales with a total dollar value of $46 million. Whereas sales of single-family homes had got back to 2005’s level by 2021-2022, land sales are still well below the levels of 2004-2006.

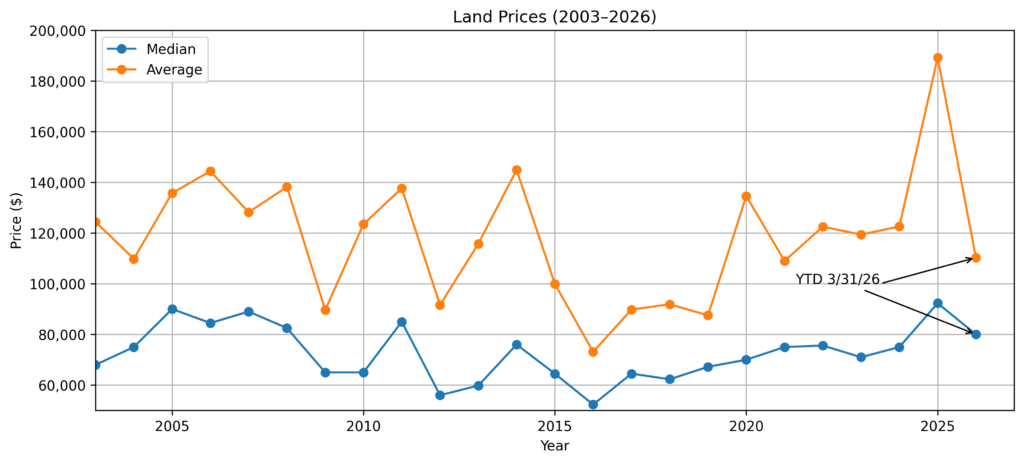

Price Level – Note: The median price—the price at which there is an equal number of sales above and below– is a better measure of the overall price level than average price. The average price (total dollar sales divided by the total number of sales) can be skewed by several extremely high-priced sales, and also by relatively more sales in the higher price brackets in one year compared to another year..

Median price for 2026 Q1 was $80,000 vs. $125,000 in 2025 Q1. That’s a decrease of $45,000 (-36.0%). There were more sales in the higher price brackets last year in the first quarter. For full year 2025, the median was $92,300.

Average price so far this year is $110,300 compared to $195,000 last year for the same time frame, which is $84,700 less (-43.4%). Again, last year saw relatively more sales in the higher price brackets (above $250,000) during the first quarter.

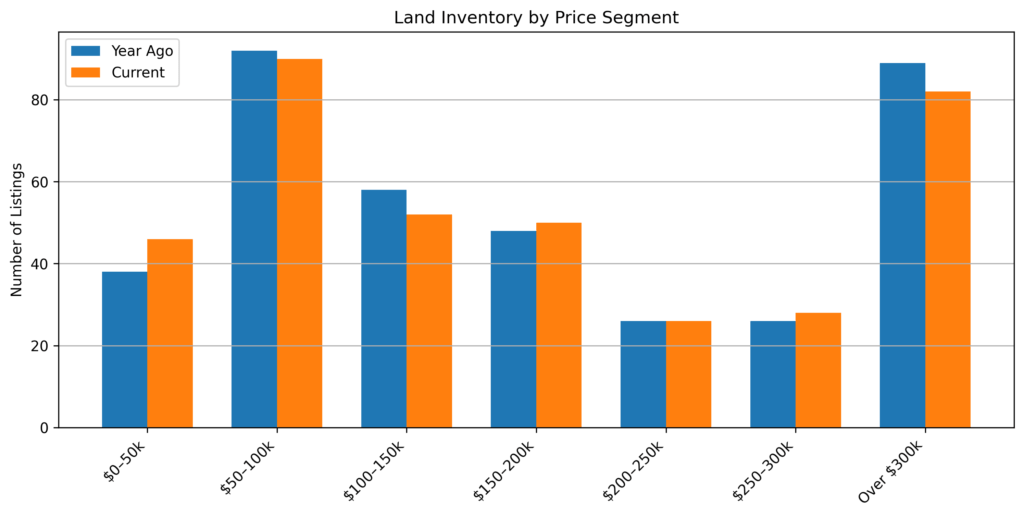

Current inventory of 374 tracts listed for sale is within the 350-450 range that has been typical for most of the past 20 years. At the current absorption rate, 374 tracts equals a 3.7-year supply, i.e., much more supply than demand.

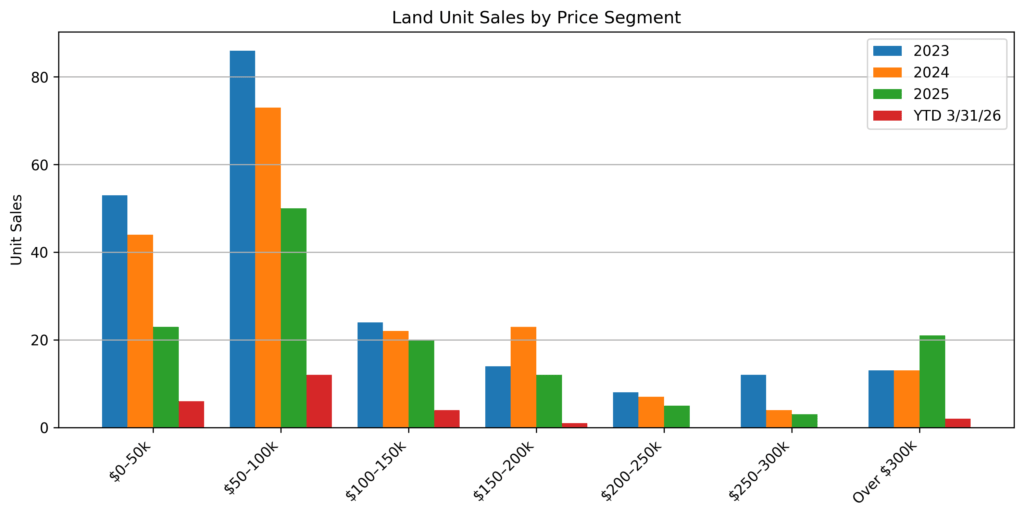

INVENTORY AND UNIT SALES BY PRICE SEGMENT

PRICE DISCOUNTING

For the first 3 months of 2026, actual selling price averaged 7.6% below the last asking price when the property went under contract; the discount from original price when the land was first listed 11.3%. For full year 2025, these discounts were 11.5% and 15.6%, respectively. Once again, we must state that with a small data set of only 25 closed sales, it is premature to draw conclusions.

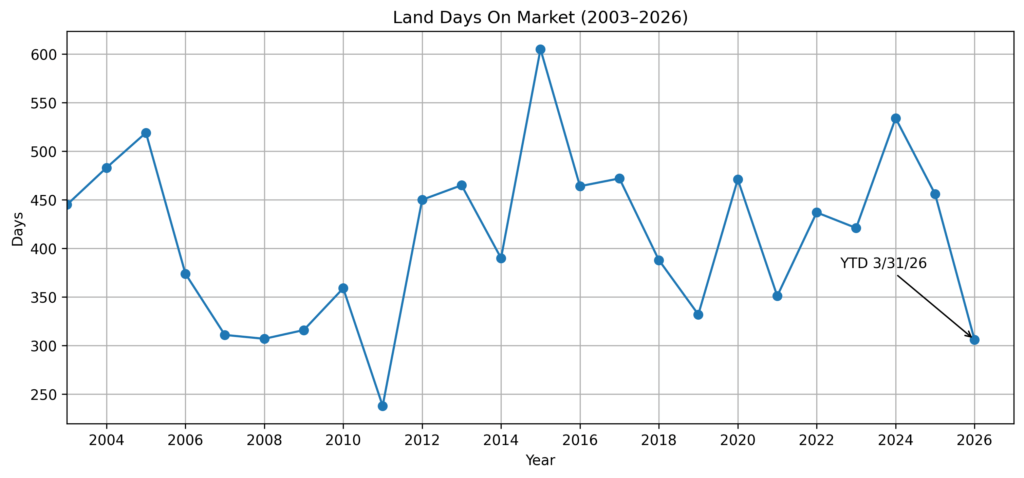

DAYS ON MARKET

The average days on the market for 2026 Q1 was 306, a decrease of 71 days (-18.6%) from 2025 Q1; this is also well below the full-year 2025 average of 456, and the 2024 average of 534. As the chart below illustrates, DOM for land has varied from a low of 332 to a high of 605 over the past 12 years; the average is 443.

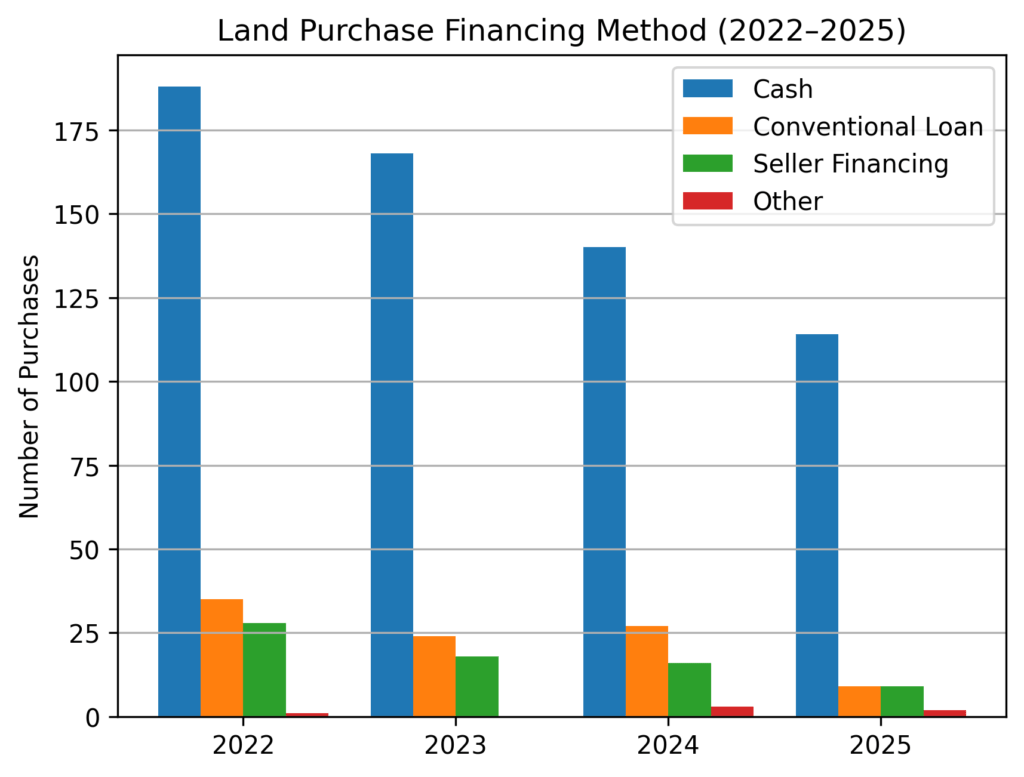

How Land Purchases Were Financed

Cash has always been the primary way that Land purchases are financed. Back in the early 2000’s up to the Great Financial Crisis of 2008, land financing through banks was more common; in fact, land loans were available through some mortgage brokers. After the GFC, lending standards tightened a lot, and land financing became more difficult—and more expensive—to obtain. These days, land loans are usually handled by commercial banks in the local area. Such loans typically require a down payment of 30%-35%, and are made for a term of only 5-7 years.

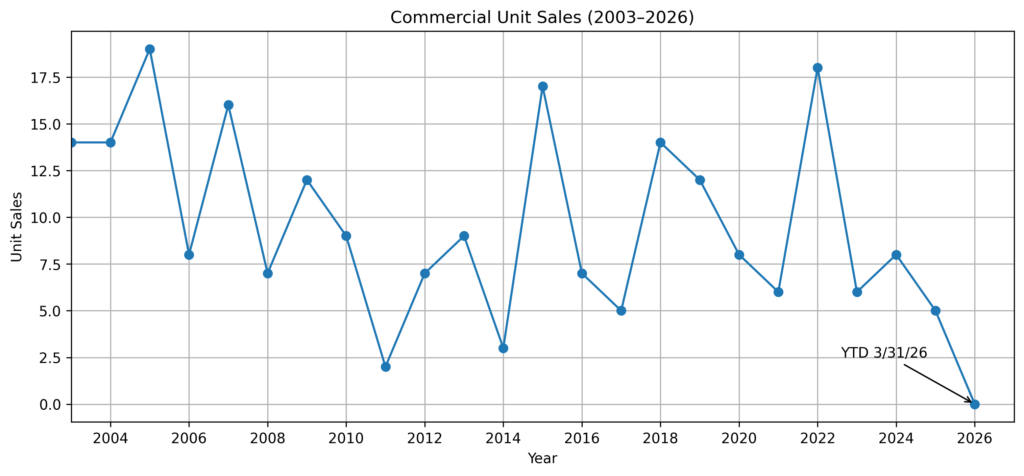

The were no commercial sales in the first quarter of 2026

2025 Q1 sales were also nil. For the full year 2025, there were only 5 closed commercial transactions, a decline of 3 sales from 2024. After a boomlet in 2022—when there were 18 closed sales— the commercial market has come down to a more typical level for Taos (i.e., small). The chart below shows that 6-8 commercial transactions per year has been the norm. The 2022 boomlet was driven by demand for locations for cannabis retailers as soon as the State of New Mexico legalized recreational marijuana sales.

2026 sales will probably be about the same as 2025’s. The commercial market is negatively affected by the higher interest rates that have prevailed for the past two years. As with multi-family property, higher interest rates affect potential return on investment, and/or the buyer’s ability to qualify for a loan. Additionally, misgivings about the health of the economy, and an ongoing shortage of labor, have made commercial investments less attractive. However, there is some commercial development happening, including a second Cid’s food store, an expansion of the Town’s only car dealership, and another self-storage facility, to name a few.